Modeling Tuck-in M&A

The following paragraphs and exhibits provide a framework for how to model tuck-in M&A from first principles, as well as a discussion on the rationale for each step and how this transaction links into the Six Core Schedules of the base LBO. Follow these steps to build Tuck-in M&A into a model outside of Mosaic (i.e., in Excel). For an Excel copy of the below analysis, reach out to your Mosaic Account Executive or sales@mosaic.pe.

A digital Tuck-in M&A model is available in Mosaic under “Special Situations” to save you from needing to repeat these steps and reduce manual error. See our help article below on how to add tuck-in M&A to your Mosaic model:

Mosaic Special Situations | Tuck-in M&A

Tuck-in M&A impacts the following schedules:

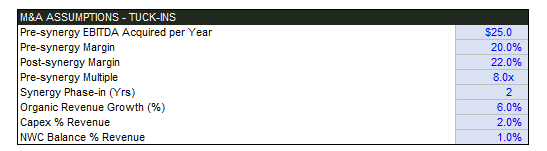

Step 0 – Tuck-in M&A Assumptions

As with any deal modeling exercise, it’s helpful to start by setting up an assumptions bank that clearly separates your chosen inputs from the mechanics of the model itself. The key assumptions you need to make space for before building anything are:

Pre-synergy EBITDA Acquired per Year. The EBITDA you will acquire each year before accounting for any synergies.

Pre-synergy Margin. The margin (i.e., EBITDA / Revenue) at the time of acquisition – again, before accounting for synergies.

Post-synergy Margin. What the margin rate will be after expected synergies are realized.

Pre-synergy Multiple. The average EBITDA acquisition multiple for the tucked-in businesses.

Synergy Phase-in (Yrs). The number of years it will take to realize the synergies on acquired businesses.

Organic Revenue Growth (%). The annual growth rate of the acquired businesses.

Capex % Revenue. The capital intensity of the acquired businesses (impacts cash flow).

NWC Balance % Revenue. The Net Working Capital profile of the acquired businesses (impacts cash flow).

Here’s an example of what the Tuck-ins Assumptions bank looks like in Mosaic’s Excel download:

Step 1 – Setting up the M&A Tab

Modeling Tuck-in M&A is a fairly involved exercise worthy of a separate space (ideally a tab) in your model to lay out all the necessary analyses. While M&A will impact and link through many of the existing Six Core Schedules of the base LBO, you will need to create the following additional schedules:

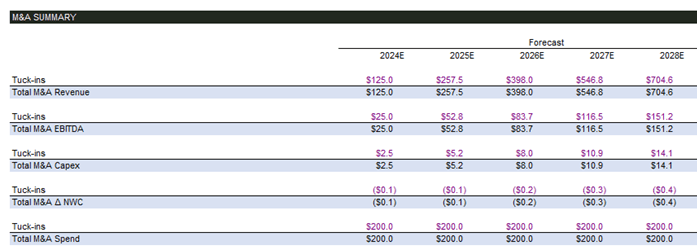

A. M&A Summary. Set up a space in your analysis to summarize the impact to the Core Four Operating Model Lines (e.g., Revenue, EBITDA, Capex, and Changes in NWC), as well as one line for total M&A Spend, which is the amount of capital deployed each year to acquire the tuck-in businesses. We will pull these values in later from supporting M&A Cohort schedules discussed in depth below. Note that in Mosaic, we set up a subtotal line for tuck-ins to support M&A modeling for both tuck-ins and transformational M&A within one model – if you only need one type, you can simply create the blue highlighted rows below:

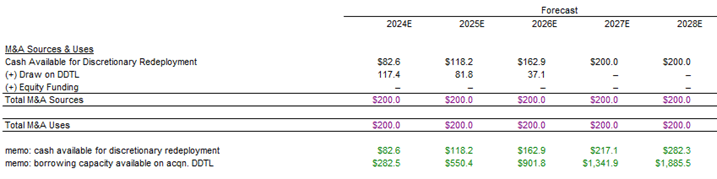

B. M&A Sources & Uses. There are three main ways for a Platform to pay for tuck-ins: (i) Free Cash Flow, (ii) Additional Debt, or (iii) Equity – almost always in that order of preference. Set up a schedule to track how each dollar of M&A spend is financed across these three categories:

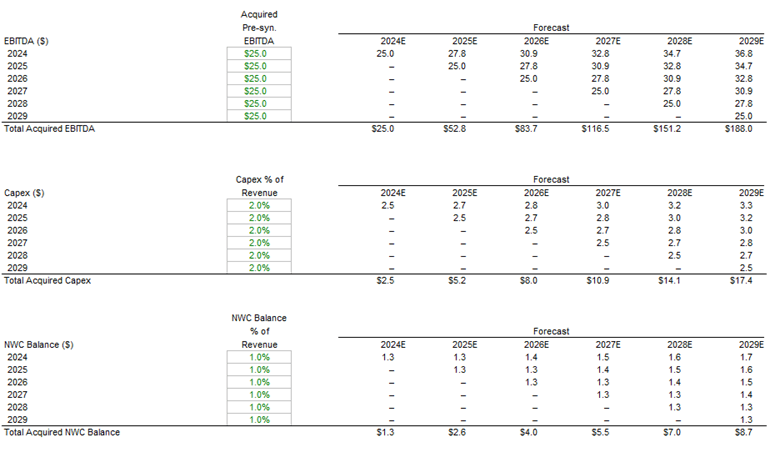

C. M&A Cohort Schedules. Here lies the core calculations for modeling Tuck-in M&A. Colloquially referred to as “M&A Triangles” because of their distinctive shape, these schedules help us to lay out the Revenue, EBITDA, Capex, Changes in Net Working Capital, and M&A Spend for each year of our hold period. Let’s first look at the Revenue section:

Each of the five lines listed above (and summarized in Step 1A) requires its own “triangle” analysis. This is because for each year of our acquisition hold period, we assume we will be acquiring some cohort of businesses – it doesn’t really matter how many individual businesses we acquire for the purpose of the analysis – but rather how much total revenue, EBITDA, capex, etc. we acquired and at what price. Mosaic is set up to build all this out with the minimum number of inputs – just a pre-synergy EBITDA amount acquired each year and a margin percentage to imply the revenue.

We also include an optional Organic Revenue Growth rate, as some sponsors want to further assume that the EBITDA they acquire each year continues to grow during their hold period.

For each triangle – set up your normal forecast years as columns, but also set up the forecast years as row labels extending down in ascending order. Each of these rows will represent a “cohort” – i.e., a group representing the businesses purchased in the year denoted on that row’s label (e.g., in the case above, 2024 for the first row). The way to read the exhibit above is that “in 2024, we acquired businesses generating $125 million of combined revenue. In 2025, they grew revenues to $132.5 million (i.e., same row, one column to the right), then $140.5 million, and so on.”

Moving down to the next row, you’d continue: “in 2025, we of course had no revenue to show for 2024, since the 2025 cohort of revenue would only come online in 2025, and would be zero before.” This is what creates the triangular shape of the schedules – because each row’s cohort only comes online in the subsequent forecast year, producing an increasing number of leading “zero” entries.

In Mosaic we set up a column for the relevant assumptions driving the Cohort schedules to make it clear to the reviewer where the key assumptions are coming from. The implied revenue is simply the acquired EBITDA divided by the EBITDA margin. Here’s a GIF illustrating the key formula behind the Revenue triangle:

An intimidating formula for sure, but all we’re saying here is:

If we’re in the same forecast year as the cohort year, it means it’s the year this cohort first came online, so just set the revenue equal to the amount initially acquired (in this case $125 million);

If we’re in a later forecast year than the cohort year, let’s apply the growth assumption to the previous year’s revenue within this cohort; otherwise

We must be in an earlier forecast year than the cohort year, so set it to zero because nothing has happened yet for this cohort.

That’s it! Simple enough.

Next up is EBITDA. In Mosaic we give the user the power to set a pre- and post-synergy EBITDA margin, allowing the user to model margin improvement (presumably from synergies) throughout some phase-in period within the hold period. The GIF below shows our math supporting the margin expansion calculation by cohort:

The next schedules are comparatively simpler: EBITDA dollar amounts are simply the multiplication of the Revenue amounts and the EBITDA margins, by cohort and by year. Capex is simply driven as a fixed percentage of revenue for each cohort, as is the NWC balance.

Remember, however, that we need to translate the NWC balance into a Change in NWC which impacts the cash flow statement by taking the difference between the balance amounts. The GIF below shows our math which has an important nuance – because we’re acquiring NWC Balances, the change from year zero to year 1 would be massively overstated unless we made an adjustment – what we do in Mosaic is “deflate” the acquired NWC Balance by the organic growth rate assumed for the acquired businesses, which results in a normalized year 1 changes in NWC:

Step 2 – Set up Acquisition Delayed Draw Term Loan (“DDTL”) Facility

Impacts: DEBT

In order to support the flexibility of borrowing more debt to fund some portion of acquisition spend, we need to set up another tranche of debt called the “Acquisition DDTL.” Doing so requires setting up an additional set of assumptions, as follows:

Let’s quickly review each:

Max. Total Leverage. This is the maximum leverage (debt) multiple of EBITDA (or whatever relevant metric for financing your deal) that the company would be able to draw up to on the DDTL.

Maturity (Years). This refers to the length of time until the newly raised debt must be repaid. Its only practical relevance in modeling is for amortizing the financing fees through the tax schedule.

Rate / Spread. This refers to the interest rate applied to the debt drawn on the DDTL. Can be fixed (stated as a percentage) or floating (stated as a basis point spread to some reference rate like SOFR).

Floor. In the context of a floating-rate loan, a floor is the minimum interest rate that must be paid, regardless of how low the reference rate (e.g., SOFR) might fall.

U.W. Fee (%). This is a fee paid to the financial institution(s) that arrange and underwrite the debt financing. The fee compensates the underwriters for their services in structuring the deal, marketing the debt to investors, and assuming some level of risk.

OID (Original Issue Discount). This is a form of interest that is incorporated into the pricing of the debt at issuance. Debt issued at an OID is sold at a discount to its par (or face) value, and the difference between the issue price and the par value is effectively additional interest income for the lender and financing fees for the borrower over the life of the debt.

Set this up as a new tranche in the Debt schedule, ensuring that you link it up to your running total debt balance that flows through to the exit calculation.

You will need to set up two additional lines to track the cumulative debt at the beginning of the period (i.e., when the M&A comes online, before the draw on the acquisition DDTL), and the remaining borrowing capacity, which is a function of the max. leverage limit you set in your DDTL assumptions and the beginning of period EBITDA (i.e., the prior period’s LTM EBITDA) plus any M&A EBITDA coming online in the current period as you would get credit for this for leverage purposes. The math looks like the below:

Step 3 – Layer Acquired Business’ Operating Performance into Operating Model

Impacts: OPERATING MODEL

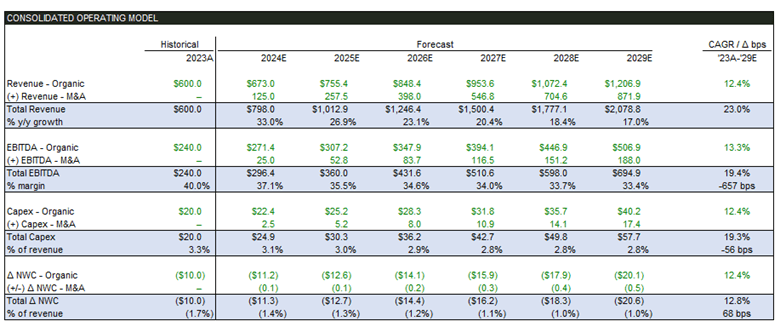

M&A impacts each of the “Core Four” rows as shown in our M&A Summary schedule. These rows need to be consolidated into our Organic Operating Model case to create a new Core Four rows that include the M&A values.

In Mosaic, we do this through a “Consolidated” tab to clearly separate out the business’ organic performance (and our assumptions around the organic case) from the acquired business’ performance. The result looks as follows:

The total Revenue, EBITDA, Capex and NWC lines shown in the blue rows would be used throughout the Core LBO Schedules in place of the Organic Operating Model lines used in a model without M&A.

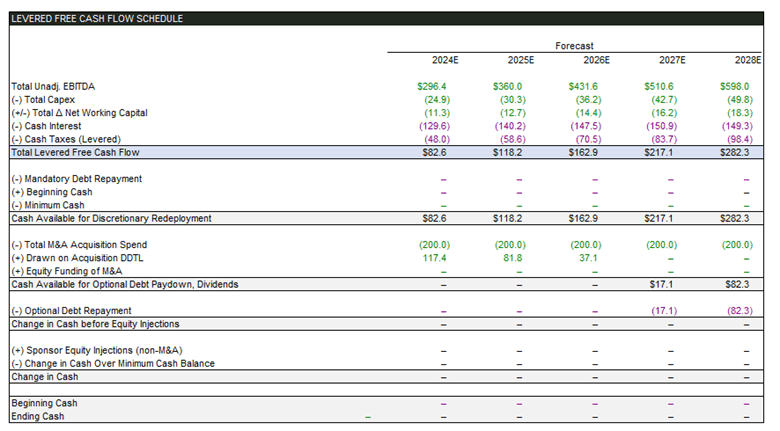

Step 4 – Layer M&A Sources and Uses into Free Cash Flow Schedule

Impacts: FREE CASH FLOW

We now need to reflect the M&A Sources and Uses amounts modeled in Step 1 into our Free Cash Flow Schedule.

We suggest doing it as follows – showing the Total M&A Spend as an outflow, and reflecting the Acquisition DDTL draw and any use of Equity funding as offsetting inflows in the Free Cash Flow Schedule:

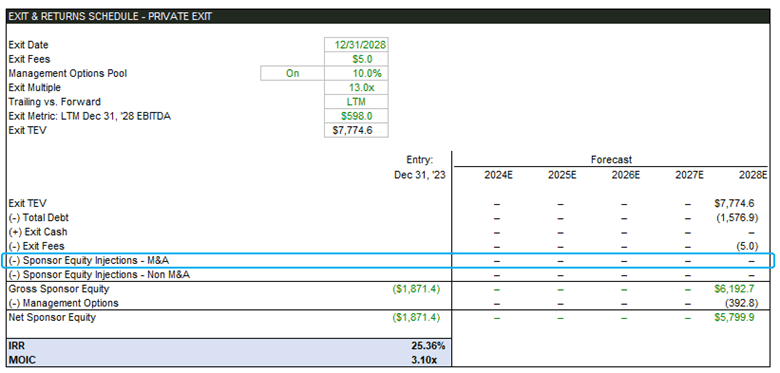

Step 5 – Link M&A-related Equity Injections Through Exit & Returns Schedule

Impacts: EXIT & RETURNS

Be sure to link through the Free Cash Flow line showing any equity issued to fund M&A through the Exit & Returns schedule – otherwise you will overstate your IRR and MOIC as you would be understating the amount of equity funded in the deal:

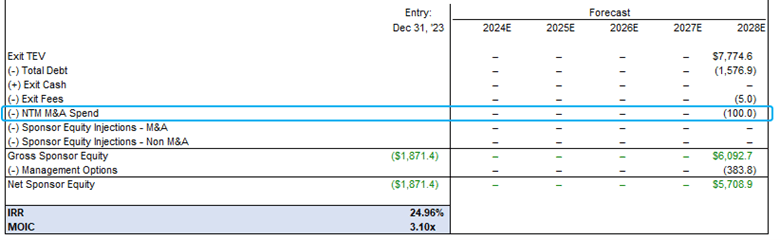

A warning: using NTM multiples in an LBO model with M&A

If you have set up your model just as we described here (which is how practically everyone does it) – that means that the EBITDA running through your model and your exit value includes the EBITDA from M&A (as it should).

However, if you are assuming an exit based off of a Next Twelve Months or “NTM” exit multiple, you would be applying a multiple to EBITDA that you haven’t yet acquired.

An example – let’s say you plan to exit in 2028 based on 15x NTM EBITDA. 2028’s NTM EBITDA is 2029’s LTM EBITDA – let’s say it’s $200 million, of which $10 million is assumed from M&A that would be acquired at 10x. The issue is that the 10x would only be paid in 2029 – so if you model a 2028 exit and give yourself full credit for the $200 million EBITDA without burdening your exit for the cost of acquiring the additional $10 million of M&A in 2029, you’re overstating your return.

In this case, we suggest making a small deduct from exit value which we call “NTM M&A Spend” in Mosaic to reflect the next year’s M&A spend as follows:

A note on “half year” M&A – the ultimate false precision

Mosaic assumes beginning of year M&A or “full year” M&A in our models – meaning that the Platform gets the full cash flow benefit of EBITDA acquired in 2024 within the 2024 forecast period. We’ve heard in the past the argument that businesses acquiring companies throughout a forecast period will likely acquire them at different times, which is best approximated by “mid-way” through the year – and therefore they should only get the credit for half the first year’s cashflows in the years those businesses are acquired.

To this we say – you have no idea when any of these businesses are going to be acquired – so January 1 is as good an assumption as June 30… and from the preamble to this Article, hopefully you know now that the vast majority of the impact from M&A has to do with the multiple arbitrage on exit, not the cash flow impact during the hold period. Making the half-year adjustment for M&A is not only false precision, it is also a distracting, value-less complexity that:

Adds another piece of calculation logic to the already complicated cohort analyses, increasing the chance of error;

Requires a “pro forma” adjustment to be added at exit, adding back the half year of EBITDA subtracted in the cash flow adjustment when applying the exit multiple to exit year EBITDA. If you forget to make this pro forma adjustment, you’re going to be misstating your exit value (important & value impacting) by a larger factor than you honed in the precision of your hold period cash flows (an unimportant rounding error); and

Obfuscates the M&A assumption – an MD reviewing a model with half year M&A may see $2.5 million of EBITDA coming online in year 1 and incorrectly assume that is the annual EBITDA acquired assumption (when it is in fact twice that at $5 million).

In the time you save not making the half year M&A adjustment – do another expert call or go for a drink with the banker running the sale process. Your deal team will be better for it, guaranteed.