Overview

Over the past two decades, the private equity industry has had an epic run of success for myriad reasons. Two of the key historical drivers of outsized returns for private equity, however, are no longer present in today’s private equity market: (i) abundant, cheap credit; and (ii) ever-expanding exit multiples, due in part to historically declining interest rates (excluding the past handful of years).

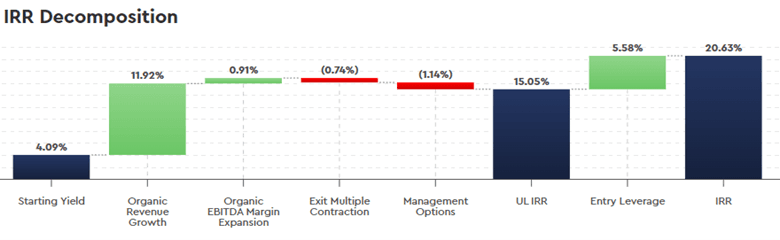

If you refer back to the categories of the IRR decomposition in Mosaic’s base LBO – the reduction of the contribution from these two levers (exit multiple expansion and leverage impact) means that in order to continue targeting a ~20% levered return on private equity deals, the shortfall must be made up from one of the other components:

So, where else can we make up for the shortfall from Leverage and Multiple Expansion?

Starting Yield. The only way to increase this number is to pay less – which private equity firms have been doing – which is why dealmaking in 2023 was so sparse. This is not entirely in a bidding sponsor’s control per se, as the seller can simply say “no” and wait for a better offer (which they also have been doing).

Organic Revenue Growth. High organic growth is extremely valuable for many reasons, and of course you want as much of it as you can get. But how much can a sponsor control this? Organic growth – particularly for the kind of large, scaled players typically targeted by private equity – is often bounded by the industry growth of the company’s end markets and its competitors’ ability to maintain market share. Fast growing companies with a high likelihood of continuing to grow fast will command a premium valuation, with the acquiring sponsor giving up from “Starting Yield” anything they gain from expected organic growth (i.e., by paying more). Again, a difficult lever to underwrite with high conviction and difficult to execute repeatably and reliably.

Margin Expansion. What we consider true organic margin / profitability expansion (i.e., not a targeted Cost Savings plan, described covered in this article) is again more so a function of operating leverage (i.e., revenues growing faster than costs) and other benefits from economies of scale (e.g., increased purchasing power / procurement leverage). Not exactly something you can bake into a repeatable 100-day post-acquisition plan.

So, what else is there? If we need a 20% return to keep up private equity’s performance standards, and we’re borrowing ~50% of the capital for a deal at ~12% all-in cost of debt these days, that means we need a ~14% Unlevered IRR (i.e., the total return before taking on any debt) to hit the bogey.

If you assume fees and management options will eat another ~2% of our returns, that means we need about a ~16% unlevered IRR pre fees and options to get the job done.

Let’s say you’re lucky enough to find a business growing mid-to-high single digits organically and by some miracle you acquire it for a 4% unlevered yield at entry. You’re maybe at a 10% unlevered return so far.

Still quite a ways to go.

So then how have private equity firms been making any money the past two years?

Mergers & Acquisitions.

M&A, roll-ups, tuck-ins, tuck-unders, bolt-ons, platforms-for-acquisitions, consolidation plays or a dozen other names for the same strategy – buy a bunch of related businesses over a period of time and sell them all as one operating entity at a later time.

Why does this create value?

It’s pretty magical, honestly, and is a beautiful example of the stuff they teach you in school actually translating into the real world.

Speaking of – let’s go back to lesson 1 of business valuation. What makes one business trade at a higher multiple than another? My key three:

Growth. A business that is growing its cash flows more rapidly than another business, all else being equal, is worth more than the slower growing business. This ties directly and clearly to the IRR Decomp and shouldn’t be controversial.

Risk. You would pay more for a perpetual cash machine if you were guaranteed that its payments would come with 100% certainty than if you did not have the guarantee. This should feel intuitive and is seen in practice with recurring revenue type businesses (e.g., SaaS) trading at higher multiples than project-based businesses (e.g., engineering services) with less visibility into future revenues.

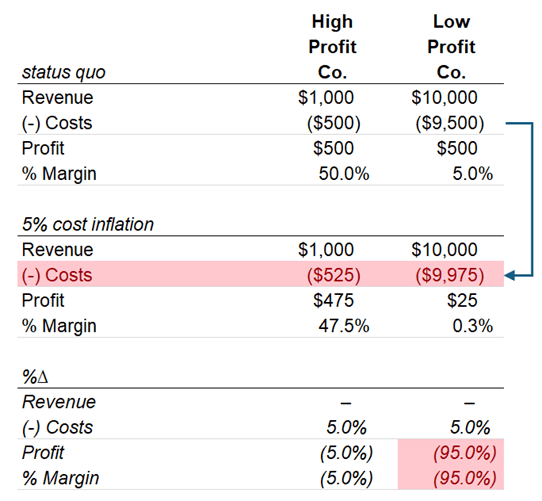

Profitability. This one is less intuitive, but I would pay a higher multiple for a high profitability business than I would for a low profitability business for a couple of reasons. First, high profitability shows that customers are willing to pay a significant premium over the productive inputs of a good or service to acquire it, which to me means the business is adding significant value to those inputs and not merely coordinating their assembly / orchestration. And if they’ve been doing it for a long period of time, they clearly have some competitive moat that have prevented copycats from eroding that margin. Second, mathematically, a high profitability business is more insulated from swings in costs than a low profitability business, which reduces the riskiness of the future cash flows (back to point #2). Here's a quick example of two companies with the same profit amount (in dollars) but significantly different profitability profiles and how they fare under a 5% cost inflation scenario:

Bringing it back to M&A

So, what does this have to do with M&A?

It’s all about bucket #2 above – Risk. Let’s say we’re a private equity firm that has just acquired a $100 million EBITDA HVAC services business focused on serving commercial customers the U.S. Northeast. The business has been in operation for 40 years, has tens of thousands of loyal customers, and employs thousands of people. The brand is well known in the region and has strong and stable market share. By this point in the business’ life, the founder probably isn’t losing sleep over their business’ right to exist. While there’s risk to next year’s earnings, there probably is no scenario in which the business produces less than $80 million of EBITDA next year – and a fairly good chance of it producing $105 million or greater.

Contrast that with a smaller operator in the commercial HVAC space serving Florida and Louisiana with $5 million of EBITDA. This operator serves only a handful of customers, and the thought of losing each one keeps the founder up at night. A local weather event (e.g., hurricane) could disrupt operations materially in any given year. A key employee quitting, or any other number of unforeseen events could easily see EBITDA reduced significantly.

Would you pay a higher multiple for the former, or latter business?

Most people would pay a much higher multiple for the former, all else being equal. Let’s say a rational investor would pay 14x for the larger business and 7x for the smaller business. How can we use this fact pattern to create meaningful value in a private equity context?

Industry Consolidators

There exist industries whose competitive landscape is made up of a handful of scaled players and a long “tail” of individual operators that combined make up a significant portion of the industry’s total revenues. This is described as being a “fragmented” industry, versus the opposite which would be considered a consolidated or even oligopolistic industry – one where a handful of large players dominate the industry and smaller players comprise an immaterial portion of revenue or are nonexistent (e.g., Digital Advertising Platforms, Smartphones, Telecommunications, etc.).

The private equity value creation play in fragmented industries is actioned as follows:

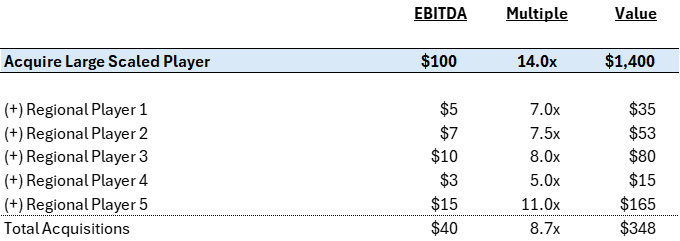

1. Acquire a large, scaled player in the fragmented industry. We’ll call this the platform for acquisitions or “Platform” for short:

2. Opportunistically acquire several subscale, regional players throughout the investment hold period:

3. Integrate (to some degree) the acquired businesses into the Platform. This could be as simple as sharing back-office functions (e.g., accounting, IT, tax, etc.) or as involved as rebranding the acquired entity with the Platform’s brand identity and transitioning all customer contracts over to the Platform’s agreements, etc.

4. Sell the combined business as an integrated system deserving of the higher, “platform” multiple applied to each dollar of EBITDA:

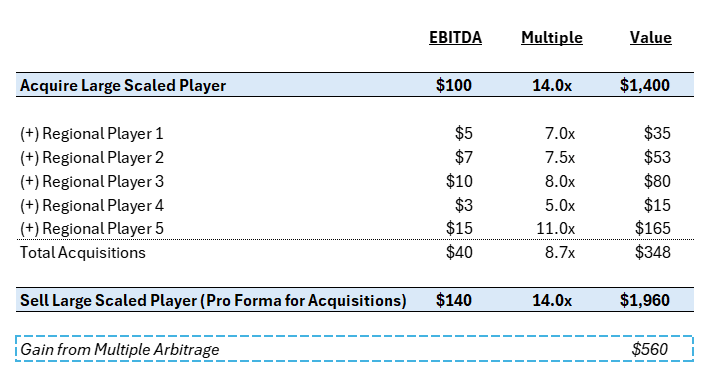

Multiple Arbitrage

The above isolates the most significant value creation lever of M&A – Multiple Arbitrage. Multiple Arbitrage is the concept of buying EBITDA for 7x and turning around and selling it the next day for 14x without doing anything to it other than packaging it alongside the higher quality, diversified EBITDA of the larger base business.

Margin Improvement from Integration

There may also be a case for the quantum of EBITDA acquired from a smaller, subscale business increasing shortly after acquisition. The reason stems from economies of scale – the acquired businesses may have redundant resources and expenses handled by the platform (e.g., accounting, IT, billing, marketing, etc.) which can result in margin expansion post-acquisition, further enhancing the value creation associated with M&A. You may hear these EBITDA improvements referred to as “Synergies” – Mosaic allows for an assumption of both pre- and post-synergy margins for acquired EBITDA to account for this phenomenon.

The only way M&A is additive from a financial perspective is if the blended multiple paid for the post-synergy EBITDA acquired is less than the multiple the Platform is sold for at exit.

Critics of Aggressive M&A

There is no shortage of critics of private equity firms for taking this approach aggressively and packaging up loosely integrated and sometimes unrelated businesses with the goal of capitalizing on multiple arbitrage. The most important thing in evaluating an M&A pipeline for a new deal or portfolio company is understanding the homogeneity of the players in the fragmented market and their industrial logic for being under “one roof” instead of remaining independent players (e.g., will customers benefit from a shared, coordinated back office and go to market motion? Are the products and end markets the same?)

Benefits of M&A

A well-executed platform for acquisitions can not only create tremendous value “on paper” through the Multiple Arbitrage math illustrated above, but it also serves an important role in the economy. Independent owner-operators of small businesses may not have a succession plan in place for their business, but deserve a way to benefit from their life’s work. Private equity has created a reliable mechanism for founders of great small businesses to capture that value. It also has the potential to serve customers better – a simple example, but do you think the customer portal is a better experience for a $100 million national business or a $5 million regional business? There are real, tangible benefits to scale that benefit not only the bottom line, but also the consumer.

Modeling Mergers & Acquisitions

There are two ways to model Mergers & Acquisitions into a deal model. The first, which we call “Tuck-in M&A,” follows the example we presented above. The sponsor makes an assumption that they will acquire some amount of EBITDA each year over their investment hold period at some assumed blended acquisition multiple.

The second, which we call “Transformational M&A,” assumes one or more large, specifically identified deals are consummated over the hold period. Mathematically the two approaches are very similar, and ultimately all that matters is the quantum of EBITDA acquired and the multiple at which it was acquired (i.e., driving the Multiple Arbitrage) – but your deal team may want to show it one way or the other.

As such, we have divided the explanation of modeling M&A into these two types and also have built Mosaic to support both types of M&A: