When we refer to Operating Models (or “Op Models” for short), we are describing the private equity industry’s standard combination of select financial data traditionally found across the Income Statement (a.k.a. Profit and Loss or “P&L”) and Cash Flow Statement of accounting reports prepared under some widely recognized accounting framework (e.g., United States Generally Accepted Accounting Principles (“GAAP”), or International Financial Reporting Standards (“IFRS”)).

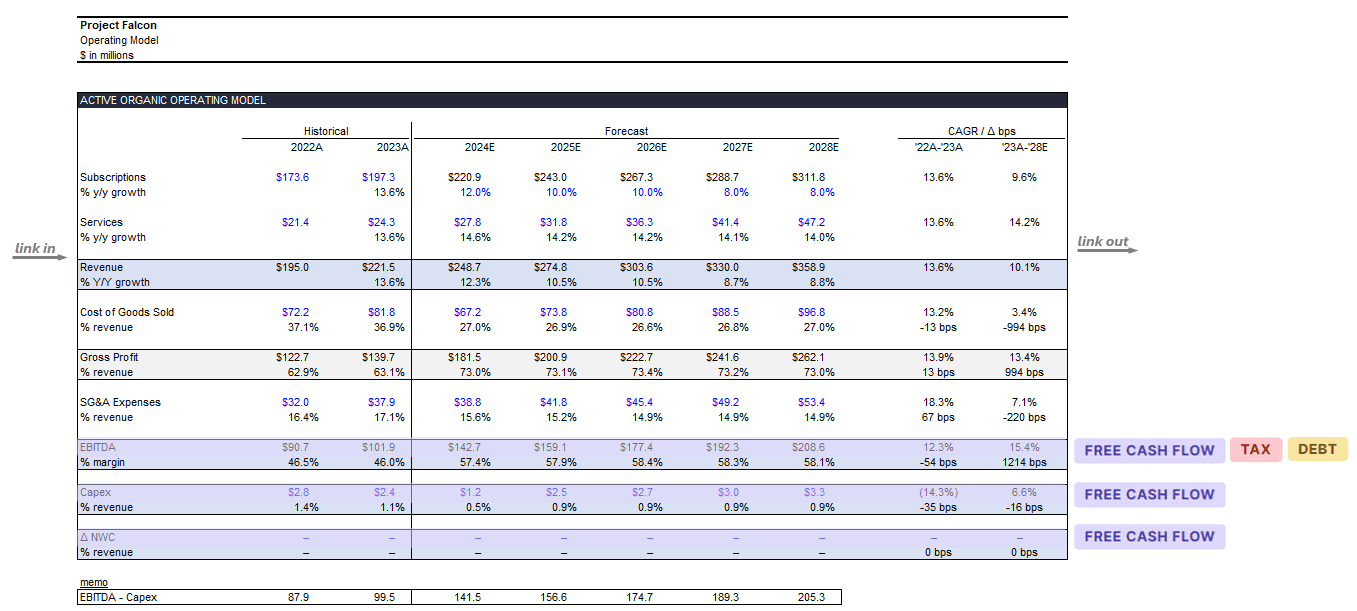

Below is an example:

The purpose for laying out financials in this format (as opposed to simply referencing the accounting statements) is two-fold:

We need to work with unlevered free cash flows as a starting point for any deal modeling (i.e., excluding any financial leverage / debt that may be on the business before our deal); and

We need the numbers on a cash basis (vs. the accrual basis that the accountants go to all that trouble to prepare for us).

The four most common lines that feed into a deal model (and therefore comprise the Operating Model) are:

The “Core Four”

Revenue

EBITDA

Capex

Changes in Net Working Capital

Dealmakers often build operating models with hundreds or thousands of lines of supporting calculations. Regardless of how much minutia you decide to go into, a standard operating business will always boil down to these four core lines (the caveat is “balance-sheet” businesses like banks and insurance carriers, which comprise a small minority of private equity-backed businesses and are not currently supported in Mosaic).

For a deeper dive into the Operating Model and detailed instructions on its construction and best practices, please see our related article: Anatomy of the Operating Model.

For a review of accounting concepts relevant to deal modeling, please see our related article: Accounting for Dealmakers.