Deal models are built to project an investor’s return over a period of time. The key output is a projected Internal Rate of Return (“IRR”) and / or Multiple of Invested Capital (“MOIC”).

Every deal model needs a minimum of five core calculation schedules spanning three distinct stages of a deal as shown below. The most common deal model used in Mosaic is the Leveraged Buyout model (“LBO”) – which is simply a deal model that uses financial leverage to fund some portion of the investment. For LBOs, a sixth schedule (Debt) is required:

Stage | 1. Transaction Entry / Set up | 2. Investment Hold Period | 3. Transaction Exit |

Schedules | SOURCES & USES | OPERATING MODEL FREE CASH FLOW TAX DEBT | EXIT & RETURNS |

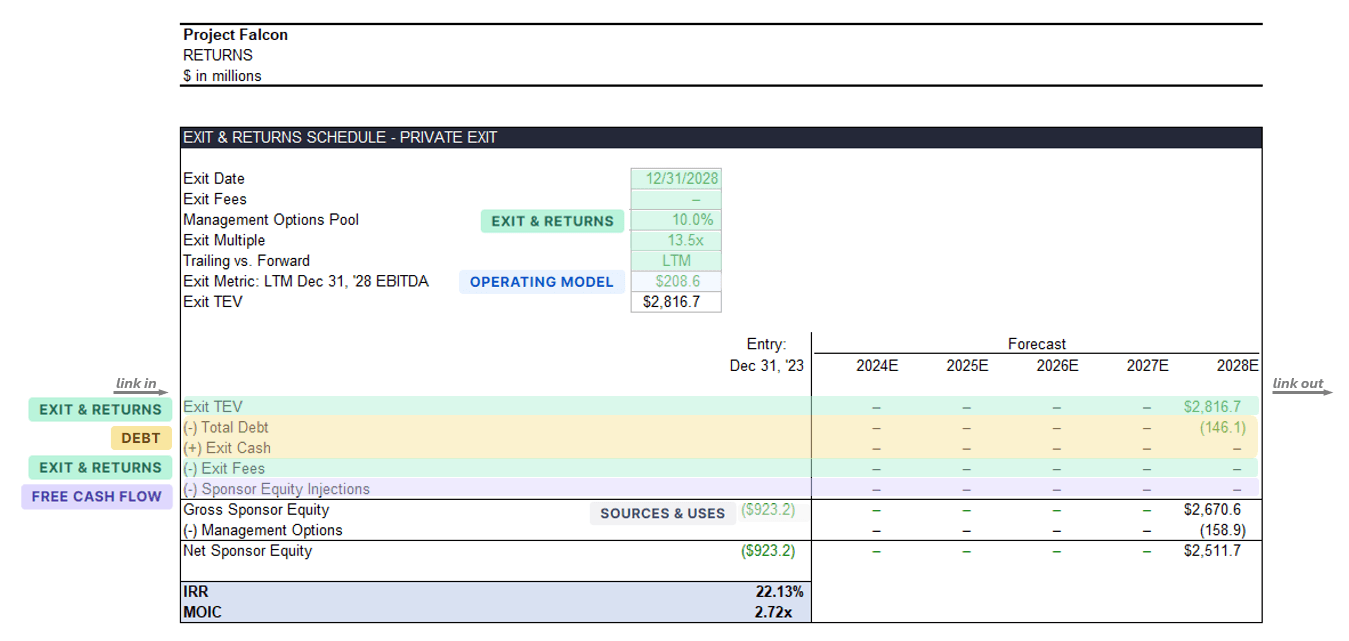

All these schedules work together to produce the Exit & Returns schedule which is responsible for computing the key IRR and MOIC metrics. To help visualize what we’re working towards, below is an example of a completed Exit & Returns schedule.

In the exhibit below, we highlight which schedule(s) each line is derived from so you can begin to visualize how the deal model hangs together overall:

This article is the first in a series discussing each of the six core schedules required to produce what we call in Mosaic a “Base LBO” (i.e., before any Model Extensions are incorporated). The series is meant to serve as a technical resource for Mosaic users interested in understanding the model deeply and how each schedule impacts the other.

Understanding this foundation will also allow you to quickly and confidently (a) understand how Mosaic’s library of “Model Extensions” each interact with the Base LBO across these six core schedules; and (b) build additional custom functionality on top of the Mosaic Excel download (i.e., if your deal situation requires some nuance not yet included in Mosaic).

The “Base LBO” is the simplest a deal model can get. It’s often more than enough model to debate “what you need to believe” about an early-stage opportunity – but soon falls short if situation-specific value creation levers are considered (e.g., M&A, Dividend Recaps, etc.) or nuanced deal timing considerations are relevant (i.e., stub entry and exit).

This series of articles should be used as a foundational reference to understand the core calculation components underlying a deal model – from which each of Mosaic’s Model Extensions build upon and future articles will dive into with reference to the impact to each of the six core schedules.