Overview

It’s hard to make an LBO work without the “L” (Leverage / Debt) – and for the past couple of years, it’s been challenging for private equity firms to pull together debt packages in the (i) size and (ii) price range of pre-2022 deals.

Because of this environment, private equity firms are increasingly underwriting Dividend Recapitalizations into their base case returns for new deals.

What is a Dividend Recapitalization?

A Dividend Recapitalization (or Dividend Recap, Div. Recap or just Recap for short) is a common financing transaction used by private equity firms that involves two steps that occur in close succession at some point during an investment hold period:

Debt Raise. The sponsor raises additional debt on the portfolio company from a group of lenders; and

Dividend Payout. The sponsor uses some or all of the debt raised to pay a cash dividend to the equity holders (i.e., themselves).

Why do a Recap?

The primary reason is to improve IRR. The overall economic value held by the sponsor doesn't materially change pre- and post-Recap – the mix simply shifts from equity value in an operating asset to cash. The cash, however, is now free to return to investors or recycle into the fund (i.e., redeploy into future acquisitions). Distributions of this nature have a positive impact on IRR as it “brings the returns forward” due to the time value of money.

A secondary reason is de-risking the investment. Less of a motivator for doing a dividend recap, but as you can see from the diagram above, there’s a bit of a “bird-in-hand” benefit to taking some money off the table early (i.e., that sliver of enterprise value “sold” to debt investors is no longer at risk for the sponsor).

What are the Drawbacks?

Additional financing fees and interest expense. While dividend recaps typically improve IRR a couple of percentage points, they also erode a bit of MOIC as they introduce more cash costs into a deal through (i) Underwriter Fees / OID and (ii) incremental interest expense from the new debt raised.

Risks associated with over-levering a business. Adding any financial leverage always adds some risk to equity holders (i.e., capital impairment).

Modeling a Dividend Recapitalization

The following paragraphs and exhibits provide a framework for how to model a Recap from first principles, as well as a discussion on the rationale for each step. Follow these steps to build a Recap outside of Mosaic (i.e., in Excel). For an Excel copy of the below analysis, reach out to your Mosaic Account Executive or sales@mosaic.pe.

A digital Recap module is available in Mosaic under “Special Situations” to save you from needing to repeat these steps and reduce manual error. See our help article below on how to add a Recap to your Mosaic model:

Mosaic Special Situations | Dividend Recap

Desired Goal

Incorporating a Recap into an LBO at a minimum will augment the Base LBO’s IRR and MOIC for the reasons noted above: (a) a portion of the sponsor proceeds will be realized earlier, increasing IRR and (b) additional fees and interest expense will be incurred, reducing MOIC (all else being equal and assuming the after-tax cost of the Recap borrowings is less than the deal’s Unlevered IRR).

The Recap is a Model Extension in Mosaic and we will discuss its impact on the Six Core Schedules of the LBO covered in our foundational article on the Anatomy of the Deal Model.

The Recap impacts the following Schedules:

Step 0 – Recap Assumptions

As with any deal modeling exercise, it’s helpful to start by setting up an assumptions bank that clearly separates your chosen inputs from the mechanics of the model itself. The key assumptions you need to make space for before building anything are:

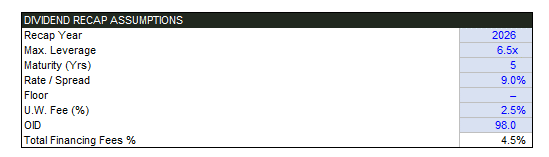

Recap Year

Max. Leverage

Maturity (Yrs)

Rate / Spread

Floor

Underwriter Fee

OID

Here’s an example of what the Dividend Recap Assumptions bank looks like in Mosaic:

Here’s a quick refresher on each concept:

Recap Year. This refers to the year during the investment hold period in which the Recap will take place. Investors typically select year 3 or 4 of the investment hold period (i.e., somewhere in the middle).

Max. Leverage. This is the maximum leverage (debt) multiple of EBITDA (or whatever relevant metric for financing your deal) that the company would be able to raise at the time of Recap. It will drive the dollar amount raised in the recap depending on the quantum of trailing EBITDA / other financing metric at the Recap Year.

Maturity (Yrs). This refers to the length of time until the newly raised debt must be repaid. Its only practical relevance in modeling is for amortizing the financing fees through the tax schedule.

Rate / Spread. This refers to the interest rate applied to the debt raised in the Recap. Can be fixed (stated as a percentage) or floating (stated as a basis point spread to some reference rate like SOFR).

Floor. In the context of a floating-rate loan, a floor is the minimum interest rate that must be paid, regardless of how low the reference rate (e.g., SOFR) might fall.

Underwriter Fee. This is a fee paid to the financial institution(s) that arrange and underwrite the debt financing. The fee compensates the underwriters for their services in structuring the deal, marketing the debt to investors, and assuming some level of risk.

OID (Original Issue Discount). This is a form of interest that is incorporated into the pricing of the debt at issuance. Debt issued at an OID is sold at a discount to its par (or face) value, and the difference between the issue price and the par value is effectively additional interest income for the lender and financing fees for the borrower over the life of the debt.

Step 1 – Set up a Recap Tranche of Debt

Impacts: DEBT & TAX

The first step to layering a Recap into your model is adding a new tranche of debt to accommodate the new debt that will be raised as part of the Recap. We strongly recommend resisting the urge to overload an existing tranche with nested formulas and complexity to accommodate the Recap – isolating it to a separate tranche is cleaner, less error prone, and makes it much easier for the rest of your deal team to review and understand what you’re doing.

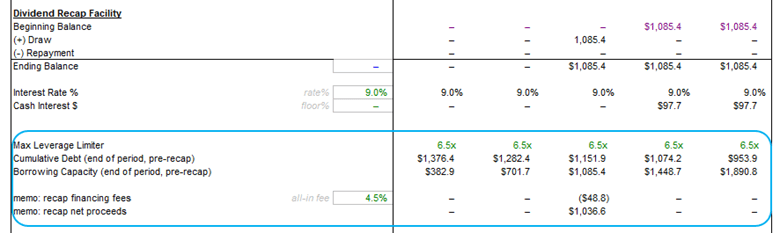

The additional tranche of debt for the Recap will look very similar to the other tranches of debt we’ve shown in this series’ exhibits or that you may have seen in Mosaic. The key difference is the five rows circled below:

These rows are responsible for: (i) testing the amount of gross Recap debt we can draw, based on our Max. Leverage assumption set (6.5x in the example above) and (ii) calculating and displaying the gross and net recap proceeds based on the Recap year we’ve selected.

Max. Recap Amount

The maximum dollar amount of debt that can be borrowed is calculated as the Max. Leverage multiple assumption multiplied by the cumulative end of period debt before considering the Recap itself. With this approach, we are implicitly assuming that the Recap occurs on the last day of the year that we selected for the Recap. This is as good an assumption as any for the purpose of an underwriting model, and is the cleanest way to implement a Recap (particularly when layering in other complexities like M&A, IPO Exits, etc.).

One of the benefits of this approach is that because we are implicitly assuming a Recap on the last day of the period, we can use that period’s EBITDA (as it would be the trailing EBITDA on the last day of the period) instead of needing to run an additional calculation of stub EBITDA for the Recap.

The Borrowing Capacity is therefore calculated as the Cumulative Debt (end of period, pre-recap) minus the Max. Leverage Limiter multiplied by the period’s trailing EBITDA (or whatever financing metric is relevant in your case). The below GIF illustrates the calculation:

Recap Draw

Next, we move up to the Dividend Recap Facility Tranche itself (lines 1-4 of the exhibit above). Set up the tranche block like we would any other piece of debt – with a starting balance of zero (we like to set it as the closing column’s ending balance and then have all Beginning Balance cells reference the prior column’s ending balance).

The only tricky bit will be the formula for the “(+) Draw” line, which is:

=IF( Current Period = Recap Year, MAX(Borrowing Capacity,0), 0 )

Lots of keystrokes to say simply: if we’re in the Recap Year, use the full Borrowing Capacity, assuming it’s a positive amount.

Below is a GIF of the formula:

The repayment line functions the exact same way as any other tranche of debt. For more information on its calculation, see our article on the Debt Schedule.

Net Recap Proceeds

As a last piece for Step 1, with the drawn amount flowing through the Recap tranche in the Recap Year, we can move on to the final two lines of the new tranche. Here, we want to calculate the cash fees payable on the recap and the net recap proceeds the sponsor will receive.

Simply multiply the “(+) Draw” line by the all-in financing fee rate (both Underwriter Fees and OID – computed as (UW Fee % + (100 - OID / 100)) to arrive at the Recap Financing Fees.

The Recap Net Proceeds are therefore the gross Recap amount (reflected in the “(+) Draw” line) minus the Recap Financing Fees.

Clean-up

The last three housekeeping items to remember before we leave the debt schedule are:

Interest. Make sure to link the Cash Interest generated on the Recap facility through the total cash interest line in the debt schedule so everything flows correctly.

Financing Fee Amortization. Make sure to add a financing fee amortization block for the new Recap financing fees you added, and accordingly ensure they are being captured by the aggregate financing fee amortization line that flows into the tax schedule.

Total Debt. Make sure to add the Recap Facility to your total debt / net debt calculations that flow through to the Exit calculations. We’ve seen many people miss this step and have to explain why the Recap was so much more lucrative than everyone would have anticipated…

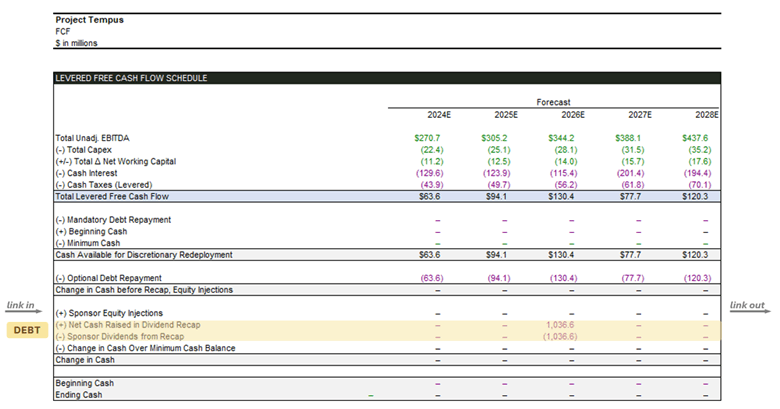

Step 2 – Flow Recap Through FCF Schedule

Impacts: FREE CASH FLOW

If Step 1 was completed correctly, the critical impact to the FCF Schedule is already automatically flowing through (i.e., the increased interest expense and reduced taxes from the interest tax shield and additional financing fees amortization).

For additional transparency and clarity for the reviewer, in Mosaic we add two display lines to the FCF Schedule to show (a) the Net Cash Raised in Dividend Recap, and (b) the Sponsor Dividends from Recap. These two lines exactly offset one another, because we assume that the Sponsor takes out the entirety of the capital raised in the Recap (which is what most investors assume when modeling this scenario). This is shown in the outlined section of the exhibit below:

Both these rows can be linked to the “Recap Net Proceeds” row in the Debt Schedule with opposite polarity.

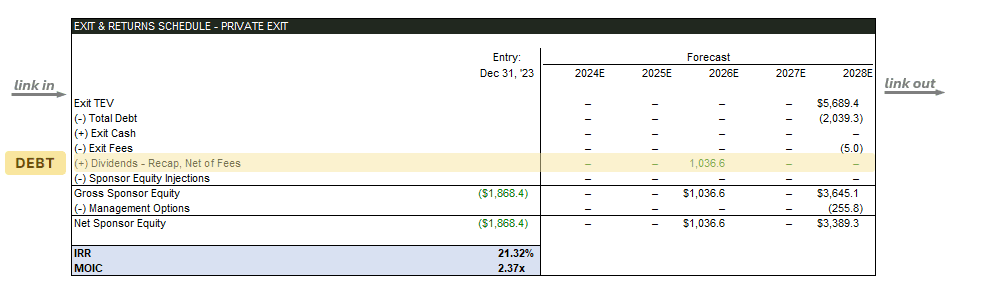

Step 3 – Flow Recap Through Exit & Returns Schedule

Impacts: EXIT & RETURNS

The most critical step that pulls all our work together is weaving the impact of the Recap into our Exit & Returns Schedule:

We insert a row into the Exit & Returns Schedule and link directly to the Recap Net Proceeds line we created in the Debt Schedule. You see from the above that this positive inflow drops directly down to the Net Sponsor Equity Row, hitting the IRR calculation directly and – in our case above – impacting IRR positively by 1.33% and MOIC negatively by 0.12x: